COVID has been with us for more than year. It has been a challenge in many ways in terms of social gatherings, ensuring the health of those dear to us (and everyone else), economic prosperity, etc.

About three years ago my colleague – Eliah Spencer – and I had a discussion about doing things that make a difference. If we could untangle from the daily business of getting the next grant, teaching the next course, … what would we do?

Building a new world

What are the key issues to address? How about access to healthcare, food, innovation, and sustainable growth? How can we possibly address these issues? Most past approaches have been centrally organized. Not clear that such approaches are always effective. Could we imagine an approach that is citizen centric, i.e., can we empower people to address these issues themselves? What toolkits should be in place for citizens to address these issues?

When COVID showed its ugly head it was an obvious use-case. How could people participate in addressing the pandemic? As many medical students are stuck at home, could they help answer questions about the pandemic? I.e., could we recruit 100s of students to address questions that people have from the front-line, small businesses, or the general public? Could people report on their experience staying at home? and could we provide information for people at home if they suspect that may have been exposed to COVID?

EARTH-2.0 – A first experiment with COVID.

To test the potential of such an approach we organized the project Earth 2.0 – earth2.ucsd.edu – with a number of local colleagues.

Answering questions was organized as a project – co-respond. Initially, the project was organized for front-line workers. If they had questions – building support for Personalized Emergency Devices (PEDs)? Can glasses help protect you from the pandemic? etc. Answers are sent using SMS, email, … to a triage desk where it is posted for the community to pickup. Once a question is answered it is checked by professionals (MDs or PEs) to ensure that the solution is valid. The validated answers are returned to the person that requested an answer and the solution is entered into a community database. The solutions were later admitted to the mobile app – Relief Central – as a separate solution area. Relief Central is supported by Unbound Medicine as a social good. The organization is committed to enhancing and delivering healthcare knowledge through digital and mobile innovation, partnerships, and a passion for advancing healthcare. The relief central app is available for Android and IOS.

The second sub-project was Oasis. The underlying idea is to allow people to put their story on a map. Lots of people have experiences from the COVID period in terms of how their illness presented, isolation, doing new projects,.. OASIS is a mechanism to share experiences and gain new insights. Recording the experience, test results, age, other information, to allow people to see how how others in their neighborhood area doing. This is similar to a story board such as facebook for people to share their experience in terms of great things and challenges. The Oasis project is mainly designed, implemented and operated by students from UC San Diego.

The third sub-project is Homebound, which was designed to allow people to record and share their health data and be guided by best practices if they are at home ill with COVID. By providing this information it is possible for people to assist with their own medical care without having to check in by phone, video, or in person with a medical professional — and it scales much better during times when the systems is already under a heavy workload.

Details about the project and the full project team is presented at earth2.ucsd.edu

Eli: The child had its one year anniversary and is doing well. What to do next?

The year 2020 is coming to an end and it is prudent to take time to reflect on the state of life, the universe, and everything on the final day of the year.

It has been an interesting year in many ways – some good news and some challenges.

Robotics

The world of robotics has generally done well. The pandemic has accelerated the adoption of e-commerce and home delivery. The pandemic has also made the need for tele-robotics much more obvious. We have seen new use-cases such as robot disinfection, which 12 months ago was considered exotic, and now it is obvious as a business case (not clear for how long).

Logistics

One of the clear winners during COVID was the need for more streamlined supply-chains. Early on in the pandemic, there was a massive shortage of toilet paper (of all things). Later a number of other things went missing for short periods of time. Home delivery from companies such as Walmart and Amazon became an everyday business.

Amazon used to have almost half of the e-commerce sector but the market share reduced to 1/3 during 2020, as more and more retails entities entered the space (Digital Commerce 360, 2020)

Service-based food delivery, such as Grubhub, and Doordash, was suddenly entirely normal just as Americans used to go out to restaurants now they were ordering food from their favorite restaurants for home delivery.

Obviously, supply chain was also a key item for delivery of vaccines to hospitals and to ensure that testing for COVID could maintain its efficiency. Multiple places had COVID testing with results returned in 15-20 hours. Some places also started to do wastewater testing for pooled testing (UCSD, 2020). Overall the biomedical sector saw significant growth.

The big push in e-commerce was bad news for local neighborhood stores. As an avid Yelp reviewer many of my regular places closed, and in many cases for good.

Manufacturing

(source: Shutter Stock)

The economic downturn that started in late 2019 progressed into early 2020. The sector saw a reduction that was on par with the downturn during the 2009 recession (FRED, 2020). Many areas saw a relatively quick recovery. However, some areas such as automotive experienced a major downturn. Multiple automotive companies reported a 50% decline in revenue. Overall manufacturing is at the same level as it was in January 2016.

After the recession in 2009 some areas of the sector did a reset. As the recovery started back companies invested in new technology. This has resulted in China going from nowhere in robotics to being the largest market in the world, while Japan has seen limited growth over the last decade. For what sectors will we see a similar change in direction as we emerges from the 2020 downturn / pandemic?

Roadmap-2020

During 2020 we published the next version of the national robotics roadmap (ref). The roadmap brings together experts from industry and academia to consider growth opportunities and R&D needs to ensure continued economic growth. The roadmap points to major opportunities for automation as part of product customization, continued urbanization, and an ever aging society. Advances in new materials, sensors, machine learning, and user-interaction is paving the way for a new generation of robot applications across manufacturing, service, logistics, transportation, and healthcare. As we see a new administration early 2021 it will be interesting to see how/if science priorities are changing.

Economics

The stock market has seen tremendous growth over the last year despite the pandemic and the downturn during February and March. NASDAQ went up 41% during 2020, S&P 500 went up 15%, and Dow Jones Industrial Index 6%. Many people saw a big challenge in late March, but the market regained a lot of its momentum in the second half of the year.

Service, E-Commerce and new Energy did by far the best on the stock exchange, while cruise lines and oil companies fared the worst.

ROBO Global

As a co-founder of ROBO Global it was obvious to monitor the market closely, and pay special attention to the Exchange Traded Funds (ETF) sector.

ROBO Global has seen solid investments throughout 2020. The growth in logistics, healthcare, automation has generated a solid 43% YTD growth with across the various sectors.

ROBO was complemented by a healthcare investment during 2019. It would have been hard to find better timing. The HTEC fund has seen a 60% growth during 2020, as one would expect and the AUM is now well beyond $100M, and one would expect to see continued strong growth during 2021.

During 2020 a new fund focused on AI and Machine Learning (THNQ) was launched. The fund has seen a growth in value of 54% during the year. The second half of the year has been especially promising. During 2020 it was clearly shown how AI can be leveraged for optimization of logistics, quick drug discovery, real-estate optimization etc and it is clear that Artificial Intelligence and Machine Learning is a major part of our future society, so this is not surprising.

Science Community

Being a scientist / researcher during a pandemic is a different experience. We are used to spending a lot of time in meetings and at conferences. This year travel has been close to impossible. Consequently, meetings had to come to us. Doing remote meetings is not nearly as much fun and I am not convinced we have found the right model yet. We are by now used to pixelated video and sub-par audio, so volume went up and we accepted lower quality. During 2020 it became commonplace to see “strange video conference behavior” as part of commercials. It would have been difficult to imagine a year ago.

Still, science production is high. People are at home at lots of time spent in airplanes is not devoted to work in the home office. It is easy to set up 1:1 meetings between professors and students, but somethings are lost in video conferences. What will be the long-term impact on the community?

Taught two virtual classes during fall 2020. This was a lot more work that doing in person presentations and it is evident that the connection to students is very different from traditional classes. Presenting to 24 icons on a screen (where everyone has their video turned off) is much less motivating than discussing a subject with students in person. It takes a lot of work to prepare for these virtual classes and it will take time to get the model right.

An essential part of being part of the science community is social interaction, which has suffered during 2020. I think we all are looking forward to a time when we can socialize again.

R&D in a Post-COVID community?

An obvious question is how will the things evolve in a post-COVID world? It seems obvious that the educational system will slowly change to a model where engagement is life-long. For those of us in AI, Robotics, … the technology is changing at an exponential pace and there is a need for regular engagement rather than 3-year sprints. How will life-long education evolve? Could we imagine a subscription-based system where you sign up for 2-4 hours of continuing education for the rest of your life? Clearly, Coursera and Udacity have started a process in that direction, but for some domains, hands-on interaction is required a video lectures is not an obvious solution.

Others have engaged in problem-based education, where the skill and knowledge acquisition is driven by a life-long model to – learn to solve problems, learn to acquire knowledge and apply your skill set to address real-world problem. My alma mater – Aalborg University – is a leader in such an educational model and I see a need for many more to follow such a model. We do not need bit-sized education delivery, but an ability to educate people that can solve problems and acquire knowledge as the world evolves. This is especially important for areas with exponential growth.

Continuing engagement is also essential. Robotics Today (joint MIT/Stanford) and IFRR Colloquia are great examples of how the community has evolved to have weekly robotics seminars by world-class speakers broadcasted to everyone. Leading speakers could spend all their time traveling to universities to give one-hour tasks, this is a more effective mechanism for everyone to learn about state of the art, but clearly there is a need to complement with 1:1 engagement with leaders to ensure a broad model for engagement across the community.

Summary

The year 2020 has in many ways been the worst on record for most people. However, we have seen major technological progress, significant economic growth, and major changes in the academic enterprise. It will be interesting to see how we embrace these challenges and opportunities as we (hopefully) enter into a post-COVID era.

Wishing everyone a Happy New Year and all the best for 2021.

Recently the robotics industry celebrated its 60-year anniversary. We have used robots for more than six decades to empower people to do things that are typically dirty, dull and/or dangerous. The industry has progressed significantly over the period from basic mechanical assist systems to fully autonomous cars, environmental monitoring and exploration of outer space. We have seen tremendous adoption of IT technology in our daily lives for a diverse set of support tasks. Through use of robots we are starting to see a new revolution, as we not only will have IT support from tablets, phones, computers but also systems that can physically interact with the world and assist with daily tasks, work, and leisure activities.

The “old” robot systems were largely mechanical support systems. Through the gradual availability of inexpensive computing, user interfaces, and sensors it is possible to build robot systems that were difficult to imagine before. The confluence of technologies is enabling a revolution in use and adoption of robot technologies for all aspects of daily life.

Thirteen years ago, the process to formulate a roadmap was initiated at the Robotics Science and Systems (RSS) conference in Atlanta. Through support from the Computing Community Consortium (CCC) a roadmap was produced by a group of 120 people from industry and academia. The roadmap was presented to the congressional caucus and government agencies by May 2009. This in turn resulted in the creation of the National Robotics Initiative (NRI), which has been an interagency effort led by the National Science Foundation. The NRI was launched 2011 and recently had its five-year anniversary. The roadmap has been updated 2013 and 2016 prior to this update.

Over the last few years we have seen tremendous progress on robot technology across manufacturing, healthcare applications, autonomous cars and unmanned aerial vehicles, but also major progress on core technologies such as sensors, communication systems, displays and basic computing. All this combined motivates an update of the roadmap. With the support of the Computing Community Consortium three workshops took place 11-12 September 2019 in Chicago, IL, 17-18 October 2019 in Los Angeles, CA and 15-16 November 2019 in Lowell, MA. The input from the workshops was coordinated and synthesized at a workshop in San Diego, CA February 2020. In total the workshops involved 79 people from industry, academia, and research institutes. The 2016 roadmap was reviewed, and progress was assessed as a basis for formulation of updates to the roadmap.

The roadmap document is a summary of the main societal opportunities identified, the associated challenges to deliver desired solutions and a presentation of efforts to be undertaken to ensure that US will continue to be a leader in robotics both in terms of research innovation, adoption of the latest technology, and adoption of appropriate policy frameworks that ensure that the technology is utilized in a responsible fashion.

Main Roadmap Findings

Over the last decade a tremendous growth in utilization of robots has been experienced. Manufacturing has in particular been impacted by the growth in collaborative robots. There is no longer a need for physical barriers between robots and humans on the factory floor. This reduces the cost of deploying robots. In the US the industrial robotics market has grown 10+% every year and the market has so far seen less than 10% penetration. We are thus far away for full automation of our factories. US is today using more robots than it has even done before.

A major growth area over the last decade has been in use of sensor technology to control robots. More digital cameras have been sold the last decade than ever before. When combined with advanced computing and machine learning methods it becomes possible to provide robust and more flexible control of robot systems.

A major limitation in the adoption of robot manipulation systems is lack of access to flexible gripping mechanisms that allow not only pick up but also dexterous manipulation of everyday objects. There is a need for new research on materials, integrated sensors and planning / control methods to allow us to get closer to the dexterity of a young child.

Not only manufacturing but also logistics is seeing major growth. E-commerce is seeing annual growth rates in excess of 40% with new methods such as Amazon Express, Uber Food, … these new commerce models all drive adoption of technology. Most recently we have seen UPS experiment with use of Unmanned Vehicles for last mile package delivery. For handling of the millions of different everyday objects there is a need of have robust manipulation and grasping technologies but also flexible delivery mechanisms using mobility platforms that may drive as fast as 30 mph inside warehouses. For these applications there is a need for new R&D in multi-robot coordination, robust computer vision for recognition and modeling and system level optimization.

Other professional services such as cleaning in offices and shops is slowly picking up, this is in particular true given the recent COVID-19 pandemic. The layout of stores is still very complex and difficult to handle for robots. Basic navigation methods are in place, but it is a major challenge to build systems that have robust long-term autonomy with no or minimal human intervention. Most of these professional systems still have poor interfaces for use by non-expert operators.

For the home market the big sales item has been vacuum and floor cleaners. Only now are we starting to see the introduction of home companion robots. This includes basic tasks such as delivery services for people with reduced mobility to educational support for children. A major wave of companion robots is about to enter the market. Almost all these systems have a rather limited set of tasks they can perform. If we are to provide adequate support for children to get true education support or for elderly people to live independently in their home there is a need for a leap in performance in terms of situational awareness, robustness and types of services offered.

A new generation of autonomous systems are also emerging for driving, flying, underwater and space usage. For autonomous driving it is important to recognize that human drivers have a performance of 100 million miles driven between fatal accidents. It is far from trivial to design autonomous systems that have a similar performance. For aerial systems the integration into civilian airspace is far from trivial but does offer a large number of opportunities to optimize airfreight, environmental monitoring, etc. For space exploration it is within reach to land on asteroids as they pass by earth or for sample retrieval from far away planets. For many of these tasks the core challenge is the flexible integration with human operators and collaborators.

The emergence of new industrial standards as for example seen with Industry 4.0 and the Industrial Internet facilitates access to cheap and pervasive communication mechanisms that allow for new architectures for distributed computing and intelligent systems. The Internet of Things movement will facilitate the introduction of increased intelligence and sensing into most robot systems and we will see a significant improvement in user experience. The design of these complex systems to be robust, scalable, and interoperable is far from trivial and there is a new for new methods for systems design and implementation from macroscopic to basic behavior.

As we see new systems introduced into our daily lives for domestic and professional use it is essential that we also consider the training of the workforce to ensure efficient utilization of these new technologies. The workforce training has to happen at all levels from K-12 over trade schools to our colleges. Such training cannot only be education at the college level. The training is not only for young people but must include the broader society. It is fundamental that these new technologies must be available to everyone.

Finally, there is a need to consider how we ensure that adequate policy frameworks are in place to allow US to be at the forefront of the design and deployment of these new technologies but it never be at the risk of safety for people in their homes and as part of their daily lives.

The Roadmap Document.

The roadmap document contains sections specific to societal drivers, mapping these drivers to main challenges to progress and the research needed to address these. Sections are also devoted to workforce development and legal, ethical and economic context of utilization of these technologies. Finally, a section discusses the value of access to major shared infrastructure to facilitate empirical research in robotics.

The roadmap is formulated based on consultations and meeting with more than 80 people from across US and involving industry, academia and government institutions.

Over the last few months, we have seen some major changes to society. The COVID-19 Virus, or the more accurate name for the infection Sars-CoV-2, has changed many things. It has already infected more than 10 million people with 3+ million of them in the US alone (by July 2020). The global statistics is available here.

The outbreak of the pandemic has had a number of effects. First of all, the healthcare system has been challenged. People have also been quarantined at home for extended periods of time. A large number of people have been laid off in USA (and globally). In addition, people have almost stopped traveling. An obvious question is how robotics and automation can assist in such a scenario.

In the healthcare sector, there are quite a few obvious use-cases. I) there is a need to increase the frequency of testing people to get a nuanced view of the degree of infection and the speed of infections (R0). Laboratory robots allow for faster processing of samples and return of answers to people. In a city such as San Diego with 1.4 million people, the target has been to test 5,200 people every day. At that rate we could test everyone once every 9 months. Six months into the pandemic (July 2020) it is still very difficult to get a test unless you have clear symptoms. Using this strategy, we will not get solid data anytime soon. Testing of 3/1000 daily is not a tall order. Laboratory robots can automate the testing and allow for more extensive testing. Many healthcare professionals have been exposed to COVID due to their front-line jobs. As such, there is a real need to use robots to acquire samples from patients, but also to enable a doctor at a distance to examine a patient and acquire basic information such as temperature, blood pressure, pulse, etc. Using tele-presence robots it is entirely possible today to increase the social distancing between patients and medical personnel for many of the daily tasks and through this reduce the risk of exposure for professionals. There are thus many good use-cases for medical robots beyond the well-known examples in surgery.

Manufacturing has declined significantly during COVID-19 (15+%), which is partly due to changes in market needs, but also due to the economic recession gained momentum after the start of the pandemic. Total industrial production is down by 20%. We have seen automotive sales go down by more than 50% for some companies (FRED estimates a decline of 55%). When isolated at home the traffic patterns change dramatically. Retail sales was down by 20+% in May 2020 and food/drink sales were down by 50% in May 2020. At the same time e-commerce continued to have significant growth. Sales of goods in the traditional retail sector was shifting from brick-and-mortar shops to the web. During the recession in 2009 countries such as China used the opportunity to change strategy. They decided to invest in robotics. Since 2009 they have had annual growth rates between 40-50% according to the industry statistics from IFR. Initially through joint venture partnerships with companies such as ABB, KUKA, and FANUC. In addition, through launch of new robotics companies such as Siasun, GSK, and Etun. Recently, Chinese companies have acquired foreign companies such as the MIDEA takeover of KUKA. It certainly put China on the map as a major player in robotics. In the US, the annual growth in robot adoption has been 12-14% but in comparison to China with annual growth numbers of 40+% the focus has shifted towards automation in Asia with India and Vietnam as new growth nations. Today 30% of all cars are manufactured in China, will this change in a post-COVID economy? Today there is about 1 robot for every 20 workers in highly automated industrial countries such as Korea, Japan, US, and Germany and we have still a long way to go to the lights out factories, as reported by IFR World Robotics. Nonetheless, it will be important to explore how robots will serve as a catalyst for future growth in manufacturing.

E-Commerce has seen tremendous growth over the last year. The growth is both in US with major companies such as Amazon and Walmart, but also by companies such as Alibaba, JD and Tmall. Already today Alibaba with Taobao is 50% larger than Amazon and is expected to continue to grow. Amazon has deployed more than 200,000 mobile platforms in their warehouses (the number is more like 300,000 by now). In addition, we are also seeing major progress on automated object pick-up / handling with companies such as Covariant.AI, Righthand Robotics and Berkshire Grey. As people desire a minimum of contact for items entering their house, we will see higher automation at distribution centers. There is significant interest in the last-mile problem of delivering from the truck to the front door in a domestic setting. The last mile could be solved using a traditional mobile platform as seen by Amazon’s Scout, another solution is clearly humanoid robots such as digit by Agility Robotics or traditional services such as May Mobility. Leaving the ground for a minute the drone market is obviously also being considered for last mile deliveries as seen by Amazon Prime Air or the experiments by UPS.

Cleaning is another important topic. This includes cleaning and disinfection beyond the hospital and the home. iRobot has seen a major uptick in sales of vacuum cleaners and floor scrubbers during the pandemic and shares are up 65% year to date. Additional cleaning is important to many households. In addition, we have started to see a flood of UV-C disinfection robots. Using UV-C lighting it is possible to achieve a high degree of disinfection with more than 99.9% of the virus eliminated when more than 10 microwatt / cm2 is radiated onto a surface. In many cases, a high-power source is used to allow even indirect illumination to kill the virus. There are already more than 50 companies worldwide pursuing this market. UVD robots from Denmark was an early entry into the market and have sold a significant number of units worldwide. Keenon from China has developed a robot that uses both UV-C lighting and a vaporizer to disinfect an area. The vapor will get to areas that may not be directly exposed by the UV-C light and provide redundant security. These two robots are merely examples of the vast number of new robots entering this market. The first place to see deployment of these UV-C robots was hospitals and care facilities. Recently, other high-traffic use-cases such as airports have also seen deployments. One would expect other use-cases to include hotels, malls, cruise ships, and eventually, they may enter your house as supercharged home cleaning robots. This is clearly a new robotics market that we considered unrealistic just a few months ago.

Transportation has changed dramatically. Over the last decade, we have seen a change from owning your vehicle of transportation to a model where mobility as a service is becoming increasingly common. Uber and Lyft started out with drive services. Eventually, this service was extended to include e-scooters and more recently Uber Eats and similar delivery services such as GrubHub. The second-largest expense for most households in the US is related to transportation, after mortgage or rent. Through use of transportation as a service, it is possible to reduce the mobility cost and optimize for the actual needs rather than paying up-front for an expected service, in addition, parking, etc is no longer a direct cost. Recently, trucking companies such as TuSimple, UPS, Cruise, Waymo … have all started to experiment with level-4 autonomy, where the car is in charge but can request assistance from the driver. This technology has a lot of promise for both e-commerce companies and logistics companies such as UPSP, UPS, FedEx, … Transportation is a sector where results may be seen even in the short-term.

COVID has exposed opportunities for robotics from cleaning/disinfection over e-commerce to manufacturing and transportation. Robots are primarily designed to empower to people do things better, in some cases in terms of accuracy in other cases as power or sensory extensions, and access. In the aftermath of the 2009 recession adoption of robotics grew significantly. In a post-COVID world we will see new behavior patterns for social interaction, cleaning, collaboration and delivery. There are thus many new opportunities for utilization of robot technology to enhance many different aspects of everyday life.

When most people think about AI and transportation, their minds go immediately to self-driving cars. But while the delivery of truly autonomous vehicles that are safe and reliable in all environments, all of the time, remains in the relatively distant future, AI is already being applied in a variety of applications that are poised to transform our lives on the road—no matter who is doing the driving. For users of these technologies (which will inevitably include us all) and investors who are hoping to hop on board this rapidly accelerating opportunity, here are just some of the key innovations that are either here today or are just around the corner:

Smart lights Adaptive traffic lights have been improving the flow of traffic for decades by altering how often traffic lights change based on typical traffic patterns. AI is helping to take that idea to the next level with AI-managed traffic lights and streetlights. IBM’s smart traffic lights use machine vision to look at real-time traffic flow. The connected system then applies computer algorithms to determine when each signal should change to optimize the flow of traffic in real time. Similar to navigation apps like Waze, the system’s ability to analyze actual traffic rather than traffic pattern averages promises to reduce traffic congestion and commute times.

Current, a subsidiary of General Electric, is also putting the power of machine vision to work, in this case embedding AI-enabled cameras into a vast network of streetlights that do much more than illuminate streets, sidewalks, and parking lots across San Diego. Using a machine-vision camera to capture images in a wide radius around each light, the company is building a database of valuable, real-time information 24 hours a day. That information is then used to point drivers to vacant parking spots, alert police to illegally parked cars, and even identify dangerous intersections that need to be redesigned to improve pedestrian and driver safety.

Advanced driver assistance While fully autonomous vehicles may be the ultimate goal for the transportation industry, advanced driver assistance systems may prove even more useful at improving the driving experience and reducing collisions. Systems from technology providers like Mobileye and Nvidia are now available from a growing number of automakers, including Mercedes, Mitsubishi, Nissan, Subaru, and Tesla. Using machine vision, sensors, and other emerging AI technologies, these systems make it easier for drivers to park; keep them from drifting out of lanes; detect hazards such as pedestrians and stopped vehicles; recognize speed limit and other road signs; and even force a hard stop to avoid a potential collision.

Driver monitoring Texting while driving puts lives at risk, but there are many other driver activities that cause accidents, injuries, and fatalities every day. Logistics and delivery providers with large fleets—including FedEx, UPS, and USPS—are now using on-board driver monitoring systems to add a whole new level of security and safety by using AI to detect behavior that deviates from the norm. The systems can determine if drivers are texting or talking on the phone, paying attention to the road, speeding, and more. Considering that up to 75% of road accidents are caused by distracted drivers, this type of AI-enabled driver monitoring is expected to not only improve logistics efficiency, but also improve overall road safety. And don’t be surprised if self-driving trucks for package deliveries become the first fully autonomous vehicles to hit the road: the US Postal Service recently contracted TuSimple to test-run its self-driving trucks. If their efforts are successful, expect to see other commercial fleets follow quickly in their footsteps.

Smart cities Using the powerful combination of 5G and the Internet of Things (IoT) to connect and communicate across citywide networks, planners are beginning to drive vital efficiencies and improve the quality of life for residents and visitors of smart cities around the world. In Amsterdam, real-time data from the IoT is being used to monitor things such as traffic flow, energy use, and public safety, and then make needed adjustments. Smart trashcans in Baltimore and Boston communicate how full they are at any given time, making it easier to create more efficient routes for sanitation workers.

Transportation. Private transportation providers like Lyft and Uber have already put AI to work to provide riders with actual pick-up times, images of their assigned car and driver, and accurate arrival times. Using AI and 5G, they will soon be able to add conveniences such as positioning riders in the best possible locations for faster pickup and coordinating smarter driving pools. In cities across the US, AI is enabling public transportation services to cut commute times by detecting long queues at train and bus stations and using that data to increase the number of cars and coaches to reduce congestion. At the University of Michigan, the Mcity Driverless Shuttle, an all-electric bus from French automaker NAVYA, uses Lidar sensors and GPS to shuttle students across campus without a human driver. Similar systems are also tested at the Texas A&M campus

From moving people to delivering goods, AI technologies such as Lidar sensors, machine vision, machine learning, adaptive planning, and IoT are already beginning to have a dramatic impact on how we get from one place to another and how goods of all kinds are delivered from the factory floor to the consumer’s front door. AI’s ability to accelerate and innovate transportation—and the opportunity for investors to make the most of a technology revolution that is already in process—is nothing short of massive. Are you on board?

More than 25 years ago, I found myself, once again, sitting at a conference watching a presentation by a major consulting firm. But this one was different from anything I’d seen before. The video showed what was then a fantastical scene of a woman getting ready for work. Standing in her kitchen, she told her coffee maker to brew a hot cup of coffee. She turned to her refrigerator and told it to add milk to the grocery list. She then switched on her computer for a quick video meeting with her team—all of whom were visible online as they discussed the day ahead. As she headed out the door, she asked, “What’s the weather today?” A voice that came seemingly from the heavens told her to go grab an umbrella: there was rain in the forecast. As a roboticist myself, the technology didn’t surprise me; I knew everything I was seeing was available in some shape or form at the time. What did surprise me was seeing that technology being applied in the real world—and not in an industrial setting, but in the home.

Looking back, it’s almost shocking that it actually took so long for AI to find its way in through the front door. But now that it’s here, the reality is even more impressive than what I saw in that once futuristic video.

Today, there are more than 10 million AI-assisted vacuum cleaners in use, and that number is growing every day. iRobot was the first to introduce an autonomous vacuum, the Roomba, back in 2002. Its newest models include Imprint™ Smart Mapping Technology, which uses machine learning to adapt to the specific cleaning needs of each room in your home, and the new iRobot mop. iRobot’s bots can navigate around furniture; clean rugs, hardwood, and tile; and can even be voice-controlled through Alexa or Google Assistant. And while Dyson’s newest vacuum cleaner may not run so independently, it does use complex AI algorithms to determine the level of suction power needed as you clean your house. There are also AI-driven window washers, stove-top cleaners, and self-cleaning litter boxes. If there’s something that needs to be cleaned, AI is coming to the rescue.

Cleaning, of course, is just one way AI is making our homes more efficient. Amazon’s suite of Echo products, all armed with the Alexa speech interface, can now do everything from play your favorite music to control your lights, check on your family anywhere in the world via live video, manage your calendar, and order nearly anything you can imagine from Amazon. Google Home and its Google Assistant can also give you music, news, and weather on demand, and while it doesn’t yet offer the home management tools supported by Echo, it is at the ready to help do everything from start your washing machine (on the right setting, too!) to turn on your shower in the morning—before your toes even touch the floor.

AI is also becoming popular for home climate control. Products like Nest offer smart doorbells (complete with real-time video, a 3-hour recorded history of what took place on your doorstep, and even face recognition software to keep you safe), Wifi-enabled smoke and CO alarms, smart thermostats that learn what temperature you like and then build a schedule around you, as well as door locks and more.

AI is also helping to keep the elderly safe in their homes. Remote monitoring solutions are now available that combine AI and wearable devices to monitor vital signs from the comfort of the home. Other devices use AI to spot changes in activity levels and behavior patterns and automatically request help if the user has fallen or become ill. Solutions from Amazon Echo and Orbita Health support adherence to medication regimes and home healthcare routines, and virtual caregivers—which are already in use in a growing number of healthcare facilities—will soon be coming into the home to help the growing elderly population who is choosing to “age in place.”

It seems new AI-driven tools for the home are being introduced every day. Thermomix saves time by changing the way home chefs chop, steam, blend, grind, and cook entire meals. AI-enabled scales tell you not only how much you weigh, but also analyze your body fat, measure your water weight, and give you other statistics like bone and muscle mass, body age, basal metabolism, and more. And expect a new member of the family soon in the form of an AI personal assistant. Today’s winners include household robots with smart social skills, and products like the Beam System that allows you to video chat with family and friends from almost anywhere. Tomorrow’s options are likely to be better conversationalists and offer skills that will further transform your home—and your life—using the power of AI.

For investors, the growing prevalence of AI in the home presents a tremendous opportunity. Not only are the makers of each of these innovations poised for future growth, but the underlying technologies that make them possible—machine learning, computing and AI processing, sensing, actuation, voice recognition, and more—are being applied in a wide variety of products, both in the home and across a vast landscape of industries. As the focus on AI and Big Data continues to expand, so will the prospects for investors who recognize and act on this inevitable trajectory today.

(originally published at Robo-Global 25 April 2019)

For some, investing in artificial intelligence feels like banking on the unknown. The concepts behind AI can range from sounding futuristic to downright fictional. And yet, when you break down AI and explore the core technologies that drive it, look at what they are delivering today, and consider what they are capable of delivering tomorrow, it’s suddenly quite easy to grasp how AI is changing the world around us. It is these facts that make investing in AI a not-to-be-missed investment opportunity.

Back in 2009, I was the main editor behind the formulation of US National Strategy for Robotics. At the time, as the strategy worked its way through Congress and to the White House, the conversation about why robotics mattered was an easy one. In the key areas of application—healthcare, defense, manufacturing, and logistics—it was simple to understand the physical applications of robotics in the real world. And yet, it was clear even then that robotics was somewhat limited in its application because, but its nature, robotics is restricted to interaction with the physical world.

AI is a completely different story.

Since 2009, our world has been fully transformed by one thing: Big data. AI enables us to make glean value from masses of information by finding patterns within the data to elevate the decision-making process, often exponentially. The result is a new wave of AI-driven decision-making that is adding value in nearly every aspect of our lives. AI is helping retailers make better customer recommendations, customize their offerings, and improve product design, delivery, and desirability. AI is helping medical professionals save lives by enabling them to diagnose and treat diseases in its earliest stages—often before symptoms occur—and compare millions of test results to quickly identify effective treatments. On Wall Street, AI is helping fund managers find the best opportunities, using data to quickly analyze everything from macroeconomic and statistical models to industry and geographical trends. AI is giving lawyers and judges the ability to sift through information at lightning speed to make better, more informed decisions. In the oil and gas industry, AI is making it possible to drill deeper, improve rig safety, and even identity system failures before they create mechanical failures that can threaten workers and the fragile environment.

What is spectacular is that this new level of decision-making would not be possible without the use of artificial intelligence and these core technologies that are driving faster, more effective memory processing, communication, and interactions:

Big data analytics is used to examine enormous data sets to discover patterns, correlations, market trends, customer preferences, and other often hidden information to inform the decision-making process. Using predictive models, statistical algorithms, and what-if analyses, big data analytics helps companies identify new revenue opportunities, create more effective marketing, deliver better customer service, improve operational efficiencies, and drive competitive advantage.

Cloud technologies enable companies to store unlimited amounts of data and balance workloads within that data. Even more, AI and the Cloud share a fascinating symbiotic loop: the Cloud serves as the primary source of information that feeds AI networks, and AI networks continuously feed the Cloud with even more data. Already a key driver of competitive advantage and a coveted differentiator, Cloud platforms support some of the most important foundations of AI, such as cloud computing, machine learning, language processing, and more.

Cognitive computing came into public awareness when IBM’s Watson computer famously beat two human champions on Jeopardy! and claimed the $1 million first-place prize. It was a brilliant marketing campaign to bring awareness of the power of cognitive computing to the public and, even more importantly, to the leaders of industry. Today, cognitive computing is used to accelerate processes such as reasoning, natural language processing, speech recognition, object recognition, and dialog generation. According to research firm IDC, worldwide spending on cognitive and AI systems is expected to increase by more than 50% by 2021, taking total spending on cognitive computing from $12B in 2017 to $57.6B by 2021.

Network & Security is more important than ever in this ager of cyber attacks and data breaches, resulting in estimated double-digit growth from 2018 to 2023, leading to global revenue of $193.76B by 2023. As businesses strive to protect the personal and financial information of their customers and, indeed, their own reputations and futures, they rely on AI to support identity and access management, encryption, governance, risk and compliance, unified threat management, and security information and event management. Encryption capabilities are in particularly high demand to protect information stored on consumer devices and to use that information securely in the Cloud.

Semiconductors are a key component of today’s digital capabilities, enabling every computer and electronic device. While semiconductors have been around for decades, AI is driving new semiconductor designs and capabilities. Using the power of machine learning and deep learning, industry leaders are finding new ways to speed up performance and reduce power, process data as patterns rather than individual bits. This progress is the key to delivering everything from quantum computers to fully autonomous vehicles.

When we created the ROBO Global Robotics & Automation Index over 5 years ago, focusing on the broader spectrum made sense. It still does. But as the promise of AI has evolved into the new world reality of AI, it was clear that the time had come to create an index with a singular focus on AI. The result of our efforts is THNQ: an index that offers 100% pure-play exposure to companies that are investing in and delivering AI today—and changing the world as we know it. Every day, the deeper we dive into AI, the more opportunity we see.

Of course, choosing whether to invest in RAAI or AI is not a clear either/or decision. Investors who are keen to invest in the physical application of technology—warehousing, autonomous vehicles, consumer robotics—will find ROBO to be the best fit. And there is certainly plenty of exposure to AI within the ROBO index; the overlap between the two indexes is currently about 30%. For investors who are seeking pure exposure into the fast-growing world of AI that is using the power of computing to drive better decision-making, THNQ is a unique option that enhances that exposure by honing in on AI alone and positioning investors to reap the potential rewards.

At the 2018 Automatica Fair in Munich, the International Federation for Robotics (IFR) presented a preview of the annual sales statistics for the robotics sector at the CEO roundtable. The final statistics will be published by IFR in cooperation with VDMA in October.

The preliminary numbers are interesting in many ways. First of all the sales of robots increased by 29% year-over-year during 2017. The total number of shipped robots went up to 381 thousand units, of which 2/3 are sold in Asia. Combined US, Europa, and other regions only represent 1/3 of the total market.

The by far biggest increase in sales was in China where the annual growth for 2017 was 58%. The growth is not only impressive but it is increasing every year.

The Chinese salaries have increased close to 350% over the last decade, which in part motivates the need for increased automation. Also today 30% of all cars are manufactured in China, but few of them are sold internationally. There is a need to increase the quality of cars manufactured in China, which again motivates an increased adoption of robot technology.

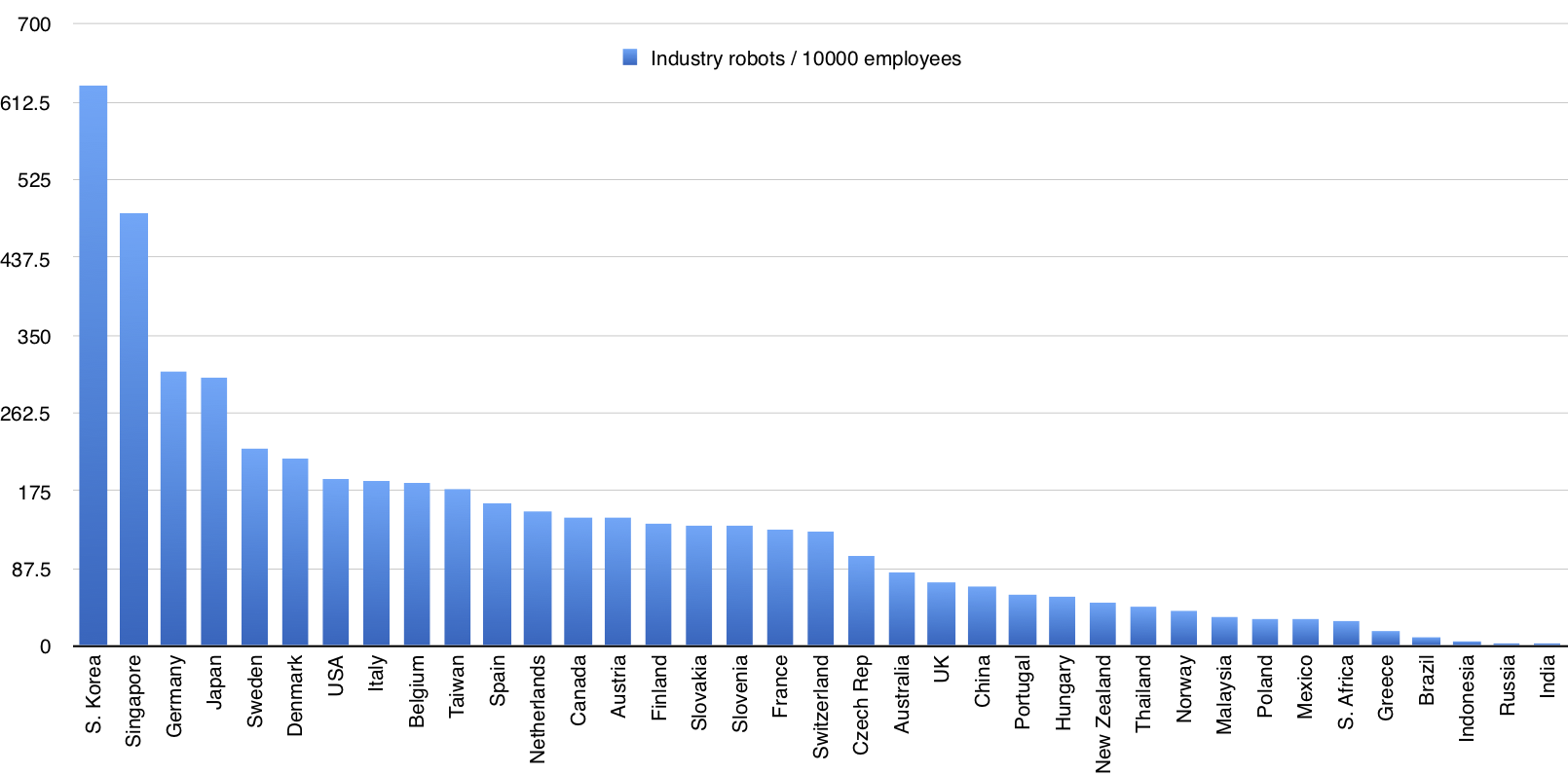

The adoption of robotics/market maturity is often measured by the number of robots deployed / 10,000 industry workers. South Korea has the highest penetration with 681 robots / 10,000 workers. The world average is 74 robots per 10,000 workers. China has 68 robots per 10,000 workers. The number has increased significantly over the last decade, but their adoption rate is still not even average and as such one would expect to a continued robust growth in adoption of robotics technology in China.

It is interesting to note that a country such as Vietnam has seen an increase in sales of 410% year-over-year which could be a direct consequence of the increased salaries in China. It is now cheaper to manufacture elsewhere in Asia and as such, there is an increased pressure on China to automate or the manufacturing will move to other countries with lower salaries.

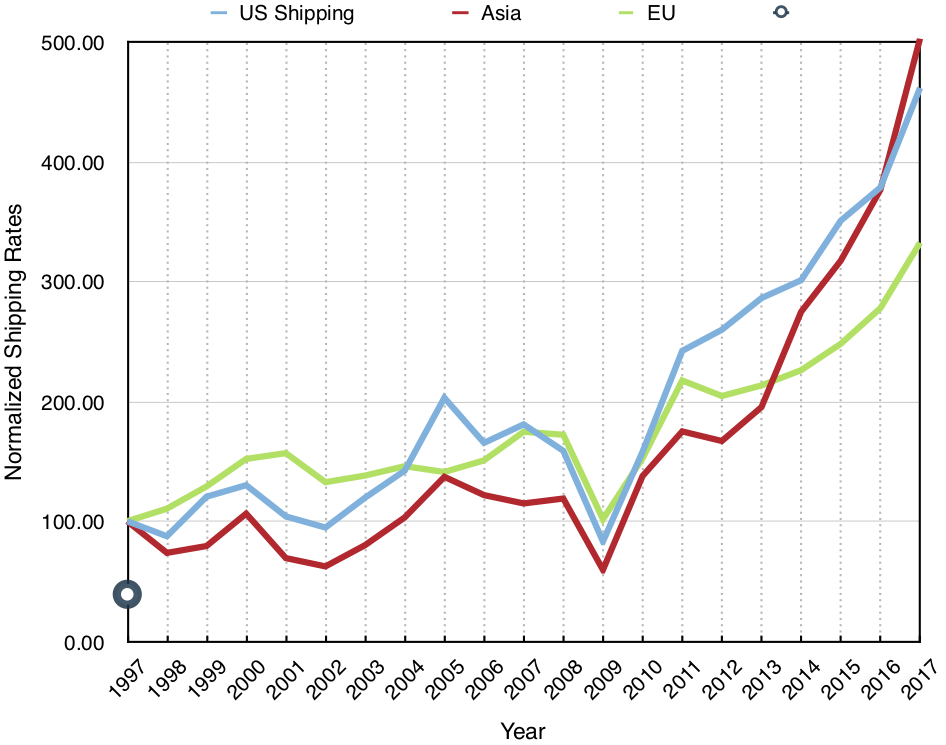

The sales figures across all regions continue to increase. The normalized sales curves since 1997 are shown below for the regions Asia, US and Europe. Every region has robust growth but it is clear that the biggest growth, in particular since 2009 are in Asia/China.

Europe saw 20% year-over-year growth, while Americas saw 22% annual growth. Other regions saw a 7% annual growth. The early numbers for 2018 do not indicate any slow-down.

Overall the manufacturing industry is seeing robust growth and there are no immediate signs of any slowdown in the utilization of robotics technology. We are also seeing an increased utilization of sensor technology to make the processes more adaptive, and the use of collaborative robots opens entirely new markets, while the use of machine learning enables faster systems integration. The integration of new technologies is expected to increase the penetration into new markets.

The first version of the National Robotics Roadmap was published 2009 with the support of CCC and later revised 2013. Just before the recent election a new version of the National Robotics Roadmap was published on November 7th.

The roadmap covers key applications drivers for use of robotics across manufacturing, services, healthcare, space and defense. Based on identified drivers the expected progress with research and development is predicted 5, 10 and 15 years into the future.

The revision of the roadmap included a re-organization of the document to have a strong separation of societal drivers and R&D needs. In addition, new sections were added to discuss educational needs, and ethical, legal and economic considerations. Utilization of new robotics technology will only be possible if we carefully consider preparation of the workforce to leverage this technology with education from K-12 through community colleges to universities. We are also seeing daily discussions about legal implications of robot technology from deployment of driverless cars on public roads to use of UAV in the National Airspace. Ethical considerations of use of robots in homes, with children, etc. are also essential to the future of robotics.

From an R&D point of view it was interesting to see that driverless vehicles and UAVs had progress faster than expected as applications. Supply chain use of robotics was also growing faster than expected. Machine learning is a technology that has gained tremendous popularity. Safe actuation, gripper technology, long-term autonomy and effective human-robot interaction are examples of areas that have progressed slower than expected.

You can read the full 2016 Roadmap here. The CCC also released a white paper earlier this year, titled Next Generation Robotics, which examines the past five years of the NRI and provides recommendations for the future.

We are at present seeing a lot of interest in autonomous systems. A lot of automotive companies are talking about autonomous cars or driver-less cars. GM and Google demonstrated early systems. Google started out with automation of regular cars and has also presented a concept system for a car without a steering wheel [URL]. Tesla has a model where the driver is expected to take over [URL] when the autopilot cannot provide a robust solution. The sharing of autonomy between well understood contexts – that are handled automatically and human intervention for challenge situation is a version of shared autonomy, where humans and robots collaborate to achieve a mission objective.

Tele-operation of robots has existed for a long-time. Much of the early work was carried out in the handling of radioactive material, where direct contact by people is not an option. These systems were all purely tele-operated. This the same type of model we see applied to medical robots such as minimally invasive systems. The Intuitive Surgical System – Da Vinci [URL] is a great example of such a system. The objective is here minimization of trauma to the body.

For Aerospace Systems we have long know the auto-pilot which is a shared autonomy system. The pilots will typically handle take-off and landing, whereas cruise flight is handled by the auto-pilot. For Unmanned Aerial Vehicles (UAVs) the pilots / operators are sitting on the ground and operating vehicles that may be airborne for as long as 36 hours. We are seeing similar applications for smaller UAVs for commercial and entertainment tasks. New commercial applications include building inspection and mapping of construction sites [URL]. For entertainment companies such as DJI [URL] build robots that are radio controlled. We are slowly seeing small functions such as level keeping or automation tracking of skiers which are examples of shared autonomy. The systems are launched and an objective is specified (tracker me, or maintain level) which is performed autonomously.

One of the biggest challenges in design systems with shared autonomy is to provide the operator with adequate context to allow them to take over as appropriate. A great example of a system that does this in an industrial context is the company Aethon [URL] out of Pittsburgh. They provide delivery robots for hospitals and other institutions. The objective is an autonomous system, but when a robot gets caught in an unusual situation such as a trashcan in the middle of a hallway, the robot requests assistance from a call center. The operator uses the on-board sensors to understand the problem and drive the robot out of the situation. If you are in a car taking over control is more of a challenge when you are driving 55 mph down the highway. It takes time to understand the challenge and to take over, which challenges the design of such systems with automatic takeover. How do we provide the driver with adequate information to take over control of the car? Or is this an appropriate model for shared control?

As we explore the shared control of systems with some functions performed autonomously and others carried out by an operator it is essential to consider the fluency of human-robot interaction, to consider the cognitive aspects of systems and to ensure that engineers use these models as an integral part of their systems design.Over the next few years we will see tremendous progress on design of systems that off-load the operator but we will be challenged in doing this in a way that still allows the operator to intervene for challenge cases. So far few systems have managed to do this with a high degree of fluency. We need more research at the intersection of cognitive science, system engineering and robotics to fully leverage next generation systems with shared autonomy.