Over the last 4 years we have seen solid growth in robot sales worldwide. The biggest growth has been in China. Overall 70% of all robots are sold in China, Japan, Germany, South Korea and USA. 25% of all robots are sold in China. The growth does not seem to stop anytime soon. Why is that?

Over the last few years we have seen major growth also in USA, South Korea and Japan. The overall sales figures from the IFR World Robotics are shown below:

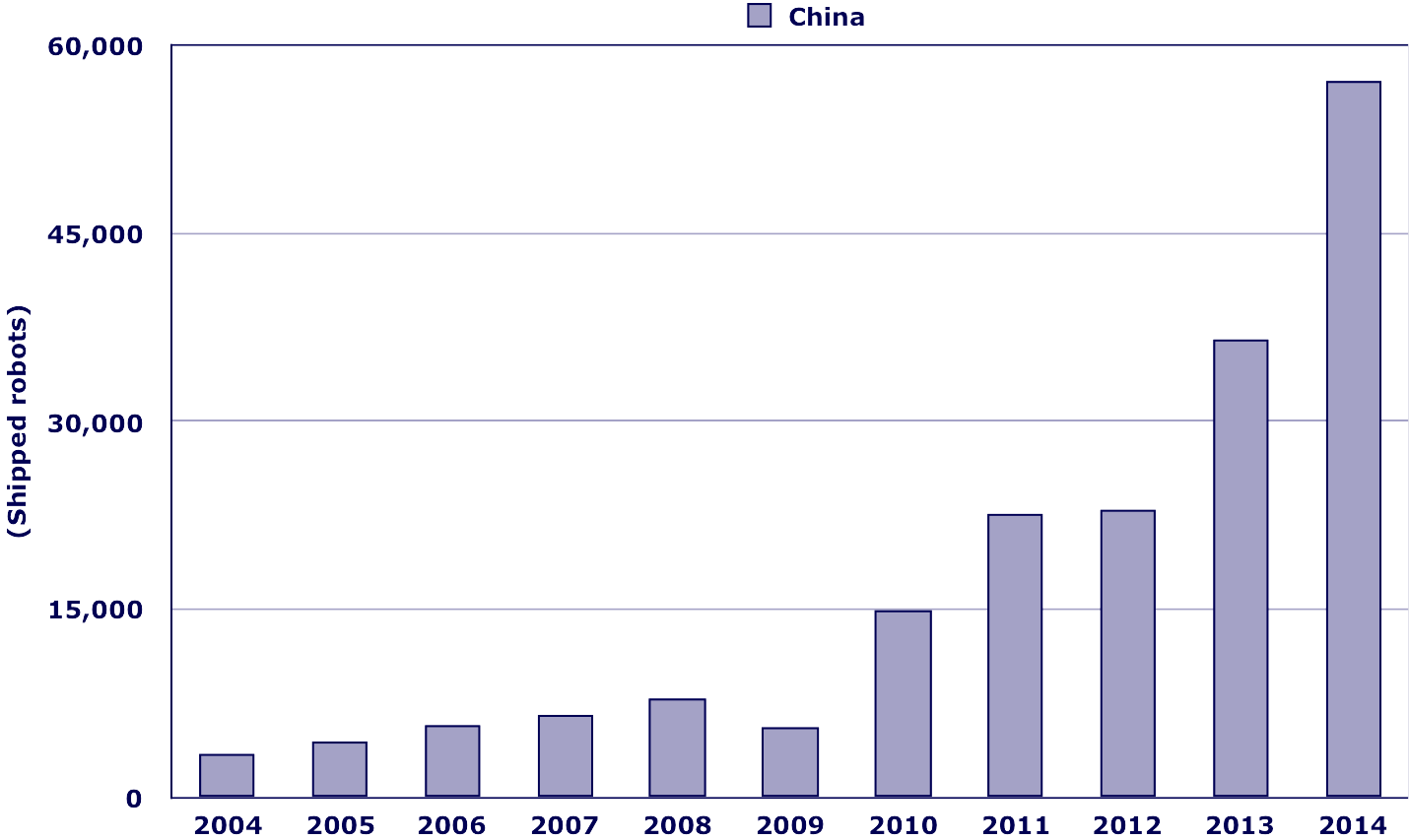

Worldwide robot deliveries over the last 10 years. The growth since 2009 is dramatic.

The CAGR since 2009 has been 17% and it is interesting that more than half of all robots sold are delivered to factories in Asia. The total value of the robot industrial market 2014 was $10B, and if integration is included the total value is close to $30B. This very much matches the general rule for cost breakdown – ~30% of an installed system is the actual robot, ~20% of the cost is related to other hardware such as the end-effector, fencing, and conveyors.

Sales in China has been particularly impressive with 50%+ annual growth that last 3-4 years. The growth has been very much motivated by a need to retain manufacturing in China. The hourly wages for manufacturing workers has gone up 350% over the last 10 years.

80% of the robots delivered were manufacturing by foreign companies or joint ventures in China. These companies experienced 49% year-year growth 2014-2015. The remaining 20% of robots delivered were made by Chinese companies. The annual growth (2014-2015) was 78% which is most impressive.

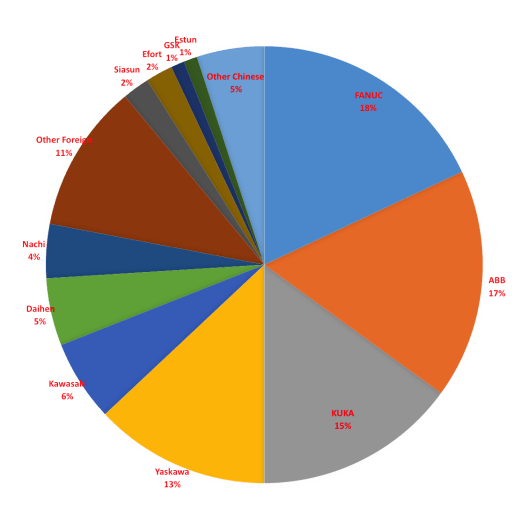

The division of market shares is shown below (for 2014). As expected the biggest company was FANUC, but closely followed by ABB, KUKA and Yaskawa. The biggest Chinese company was Siasun, that is emerging as the leader from the Chinese companies.

Already today more than 30% of all cars manufactured worldwide are produced in China. However, very few of these are sold outside China. First of all there is a major home market and in addition the industry is challenged by inconsistent quality.

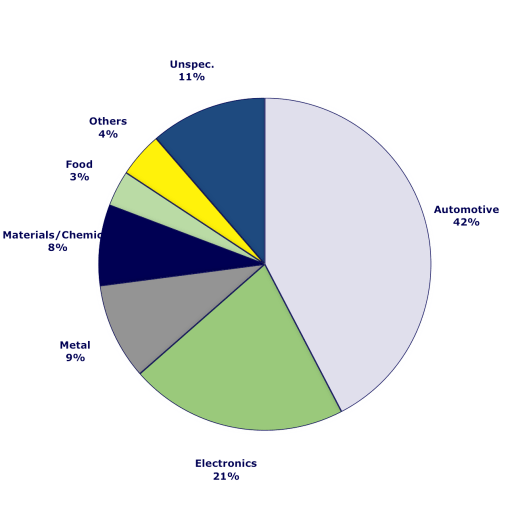

For robotics in general the main application area is still automotive, which takes up close to 42% of all robots sold. Electronics is number 2 and metal handling is 3rd. The fact that China has emerged as the largest producer of cars and also as a country with a need for automation to remain competitive points to a clear need for major growth in robot sales.

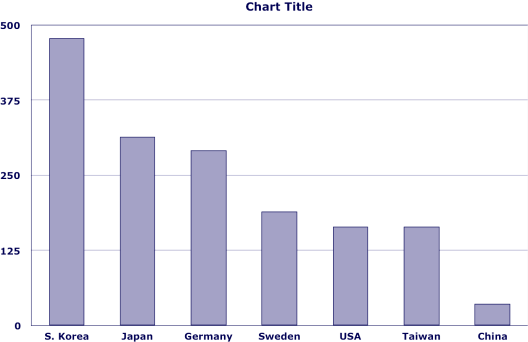

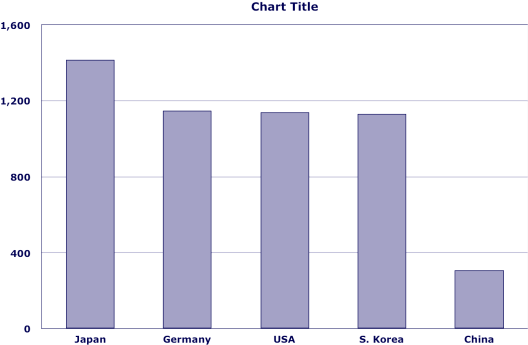

Often the maturity of a market is measured by the number of robots deployed for every 10,000 workers in an industry. Korea has emerged as a leader with almost 500 robots deployed / 10,000 workers. Japan is second and Germany third. The world average for manufacturing countries is 87 robots / 10,000 workers. For 2014 China had only ~40 robots / 10,000 workers. Consequently China would have to double its robot inventory to even have average utilization of robots.

If we zoom in on the automotive industry then the average penetration is 1 robots / 10 workers. Japan is the leader with use of lean manufacturing and a high degree of automation. Countries such as Germany, USA and S. Korea are all close to the expected 1/10. China on the other hand is closer to 1/30 as shown below.

Consequently, one would expect to see major growth for the automotive market too. Salaries are lower in China, but the real driver is really quality of the final product. The big driver is consistent quality to ensure that product manufactured at any time of the day or any day of the week have the same quality.

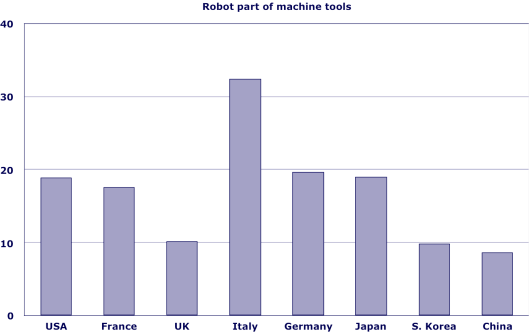

Frequently, the improvement in quality has been achieved through use of machine tools. They have a high stiffness and can generate high accuracy products with a high quality. One challenge for a factory that is laid out using machine tools is limited flexibility. It is difficult to change a factory line with a series of machine tools. In the automotive industry it is common to change the model at least annually and even with a common platform programming can be a major challenge. Consequently, we have seen an increased interest in utilization of robots as a replacement for machine tools. It is easier to change the end-effectors and industrial robots are designed for easy programming. Consequently, we are seeing a shift from machine tools to industrial robots. The general statistics for machine tools vs robots is shown below.

Again China is only at half in its utilization compares to major markets such as USA, Japan and Germany. Consequently there is no doubt we will continue to see major growth in China and slowly we will also see a strong presence of Chinese companies. In some cases these companies will emerge directly from China and in some cases these companies will emerge from foreign acquisitions such as the Midea acquisition of the majority share in KUKA AG.

Overall the robotics industry is expected to continue to see solid (~15-20% annual growth) but the major growth driver will without doubt continue to be China for the foreseeable future.

Note: Many of the numbers in the post were adopted from the IFR World Robotics Publication.

Where is healthcare in terms of robotic applications? What fraction of quarter of million robots are used in healthcare?

Rajesh, 99% of all these robots are in manufacturing. The healthcare market is quite different. The two big companies in surgery are Intuitive Surgical (ISG) and Mako Surgical now owned by Striker a major OR provider. The sales in surgical is small in comparison (by numbers) the number of arms is ~1000 or less. The robots are much more expensive but in terms of delivered items it is a small market. Some robot companies such as KUKA work with Siemens on radiation robots, … For the rehab market there is strong growth with companies such as Ekso Bionics, Johnson and Johnson, … but the number of units delivered is still small. We are seeing strong year-year growth numbers, but starting from a small place it takes time to grow the market. –Henrik